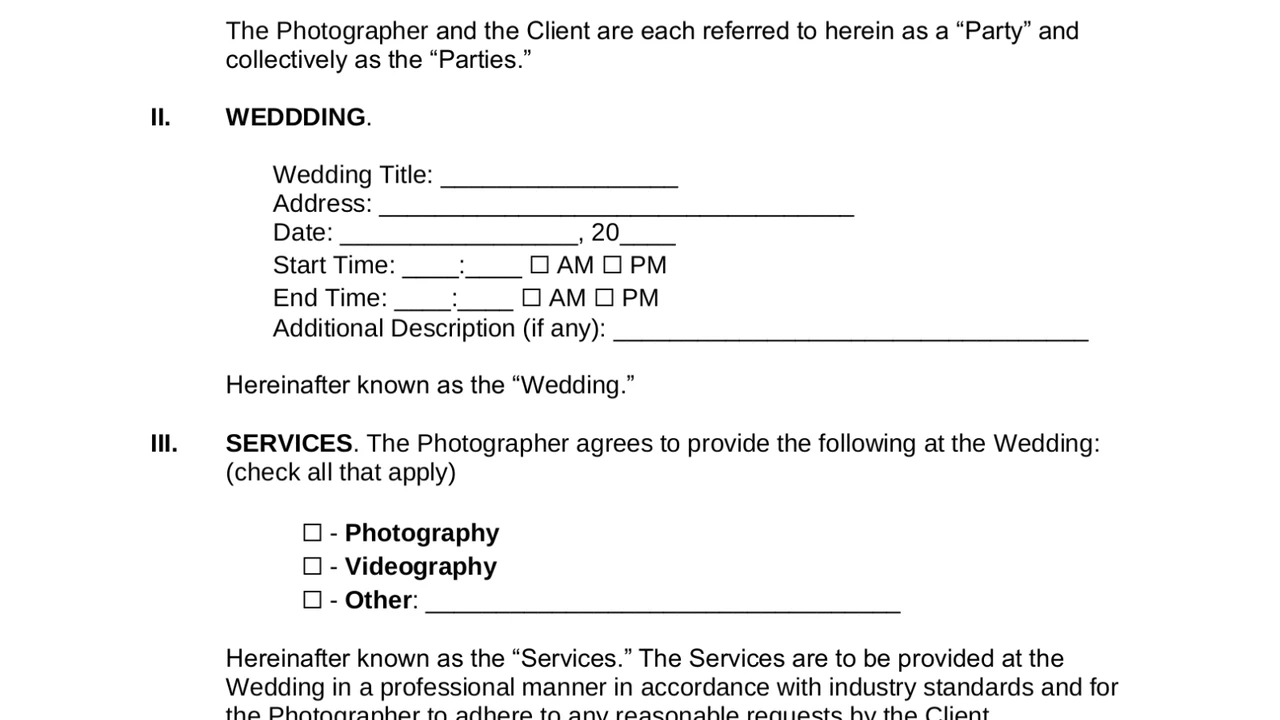

Wedding Photography Contracts: What to Look for Before Signing

Why Wedding Photography Insurance is a Must Have for Every Photographer

Okay, let's talk about something that might not be as glamorous as snapping that perfect first kiss photo, but it's arguably just as crucial: wedding photography insurance. Seriously, think of it as your safety net, your backup plan, and your "oops, I dropped the cake" contingency all rolled into one. You wouldn't drive without car insurance, right? Same principle applies here.

Imagine this: You're at a beautiful outdoor wedding, golden hour is hitting just right, and you're capturing those dreamy moments. Suddenly, a gust of wind sends a rogue umbrella flying, knocking over your expensive camera equipment. *CRASH!* Without insurance, you're looking at a hefty repair bill, potentially putting you out of business. Or, picture this: a guest trips over your light stand and gets injured. Lawsuits? Nobody wants those headaches.

Wedding photography insurance protects you from these unexpected events. It covers everything from damaged equipment and liability claims to even cancellation fees if a wedding gets postponed due to unforeseen circumstances. Basically, it lets you focus on capturing those precious memories without constantly worrying about what could go wrong.

Understanding Different Types of Wedding Photographer Insurance Coverage

So, what kind of insurance are we talking about? It's not just one-size-fits-all. There are a few key types of coverage you need to consider:

- General Liability Insurance: This is your bread and butter. It covers bodily injury or property damage that you or your equipment might cause to someone else. Think of the rogue umbrella scenario.

- Professional Liability Insurance (Errors & Omissions): This protects you if a client claims you made a mistake, like missing key shots or delivering subpar photos. Hey, it happens!

- Equipment Insurance: This covers your cameras, lenses, lighting, and other gear if they get damaged, stolen, or lost. Crucial for protecting your investment!

- Business Interruption Insurance: If a covered event (like a fire or theft) forces you to temporarily shut down your business, this helps cover lost income and operating expenses.

- Cancellation/Postponement Insurance: In the event of a wedding cancellation or postponement due to unforeseen circumstances (like illness or a natural disaster), this can help cover your lost revenue.

Which ones do you *really* need? Well, general liability and equipment insurance are pretty much non-negotiable. Professional liability is also highly recommended, especially as you grow your business. The others depend on your specific needs and risk tolerance.

Top Wedding Photography Insurance Providers Compared Pricing and Features

Alright, let's get down to brass tacks. Who are the big players in the wedding photography insurance game? And what are they offering?

- Hill & Usher (Package Choice): Known for their comprehensive coverage and customizable packages. They offer everything from general liability to equipment coverage, and you can tailor the policy to fit your specific needs. Expect to pay around $500-$1000 per year for a good level of coverage. They often have great options for add-ons like drone coverage.

- Professional Photographers of America (PPA): If you're a PPA member, you get access to discounted insurance rates through their partner insurance providers. This can be a great way to save money while still getting solid coverage. The exact cost varies depending on your membership level and coverage needs, but you can often find rates significantly lower than going directly to an insurer.

- TCP Insurance Services: Another popular option, offering a range of coverage options specifically tailored to photographers. They are known for their excellent customer service and quick claims processing. A basic policy might start around $400 per year, but expect to pay more for higher coverage limits and additional features.

- Next Insurance: Provides a quick, easy online quote and policy management process. Good for those who want to get coverage fast and without a lot of hassle.

A Quick Comparison:

| Provider | Key Features | Estimated Annual Cost | Pros | Cons |

|---|---|---|---|---|

| Hill & Usher | Customizable packages, drone coverage | $500 - $1000 | Comprehensive, flexible | Can be pricier |

| PPA (through partner) | Discounted rates for PPA members | Varies (often lower than direct) | Affordable, good for PPA members | Requires PPA membership |

| TCP Insurance Services | Excellent customer service | $400+ | Good service, tailored options | Can be less flexible than Hill & Usher |

| Next Insurance | Quick online setup | Varies | Easy to get started | May not be as comprehensive |

Remember to get quotes from multiple providers and compare the coverage and costs carefully. Don't just go for the cheapest option – make sure it actually covers what you need!

Real Life Wedding Photography Insurance Claim Scenarios What Could Go Wrong

Let's get real. What are some actual situations where wedding photography insurance can save your bacon?

- The Drunk Uncle: Yep, it happens. A guest gets a little too enthusiastic on the dance floor and accidentally knocks over your light stand, damaging it beyond repair. Equipment insurance to the rescue!

- The Missing Memory Card: You shoot an entire wedding, get home, and... the memory card is corrupted. All those precious photos are gone. Professional liability insurance might cover the cost of compensating the couple for the loss. (This is a NIGHTMARE scenario, always back up your work!)

- The Venue Fire: A fire breaks out at the wedding venue the day before the big event, forcing the couple to postpone. Cancellation insurance can help cover your lost revenue.

- The Slip and Fall: A guest trips over your camera bag and breaks their arm. General liability insurance covers the medical expenses and potential legal costs.

- The Stolen Gear: You leave your camera bag unattended for a moment (never do this!) and someone swipes it. Equipment insurance is there for you.

These are just a few examples, but they illustrate the wide range of potential risks you face as a wedding photographer. Insurance is there to protect you from the unexpected.

How to Choose the Right Wedding Photography Insurance Policy Key Considerations

Okay, so you know you need insurance. But how do you choose the right policy? Here are a few key things to consider:

- Coverage Limits: How much coverage do you actually need? Consider the value of your equipment, the potential cost of liability claims, and the amount of revenue you could lose if a wedding is cancelled. Don't skimp on coverage – it's better to be over-insured than under-insured.

- Deductibles: How much are you willing to pay out-of-pocket before your insurance kicks in? A higher deductible will lower your premium, but you'll have to pay more if you file a claim.

- Exclusions: What does the policy *not* cover? Read the fine print carefully and make sure you understand any exclusions. For example, some policies may not cover damage caused by negligence.

- Reputation of the Insurer: Choose a reputable insurance company with a good track record of paying claims. Read online reviews and talk to other photographers to get their recommendations.

- Customer Service: How easy is it to get in touch with the insurer if you have a question or need to file a claim? Look for a company with responsive and helpful customer service.

- Policy Length Annual or per-event? If you only do a couple weddings a year, per-event insurance might be a better option.

Wedding Photography Equipment Protection Insurance Specific Recommendations

Since protecting your gear is paramount, let's dive deeper into equipment insurance. Here are a few specific products to consider, along with their pros, cons, use cases, and approximate prices:

- Protect Your Bubble (Equipment Insurance):

- Use Case: General equipment protection for cameras, lenses, and other photography gear.

- Pros: Covers accidental damage, theft, and loss. Offers worldwide coverage.

- Cons: May have limitations on coverage for older equipment.

- Price: Varies depending on the value of your equipment, but typically ranges from $10-$30 per month.

- Athos Insurance (Specialized Photographer Insurance):

- Use Case: Covers a wide range of scenarios, including damage, theft, loss, and even damage during transport.

- Pros: Comprehensive coverage designed specifically for photographers. Offers options for insuring rented equipment.

- Cons: Can be more expensive than general equipment insurance.

- Price: Starts around $200 per year for basic coverage.

- State Farm (Small Business Insurance):

- Use Case: Part of a larger small business policy, can cover equipment as part of business property.

- Pros: Comprehensive business coverage, including liability and property.

- Cons: Might not be as specialized as equipment-specific policies.

- Price: Varies widely depending on coverage levels and location.

Comparing Equipment Insurance Options:

When choosing equipment insurance, consider the following:

- Replacement Cost vs. Actual Cash Value: Replacement cost covers the cost of replacing your equipment with new equipment, while actual cash value only covers the depreciated value. Replacement cost is generally better.

- Coverage Area: Does the policy cover your equipment worldwide, or only in certain locations?

- Deductible: What is the deductible? A lower deductible will result in a higher premium, but you'll pay less out-of-pocket if you file a claim.

Wedding Photographer Liability Insurance Protecting Yourself from Lawsuits

General liability insurance protects you from lawsuits if someone gets injured or their property is damaged as a result of your actions. Here are some scenarios where liability insurance can come in handy:

- A guest trips over your equipment and breaks their leg.

- You accidentally damage the wedding venue.

- You are accused of infringing on someone's copyright.

Liability insurance can cover the costs of medical expenses, property damage, legal fees, and settlements.

Wedding Photography Business Interruption Insurance Covering Lost Income

Business interruption insurance helps cover your lost income if you are forced to temporarily shut down your business due to a covered event, such as a fire, theft, or natural disaster. This can be a lifesaver if you are unable to work for an extended period of time.

Business interruption insurance can cover your lost profits, operating expenses, and even the cost of renting a temporary office space.

Tips for Saving Money on Wedding Photography Insurance Affordable Options

Insurance can be expensive, but there are ways to save money:

- Shop around and compare quotes from multiple providers.

- Increase your deductible.

- Bundle your insurance policies.

- Join a professional organization like the PPA to get access to discounted rates.

- Maintain a safe working environment to reduce the risk of accidents.

Staying Protected Peace of Mind for Your Wedding Photography Business

Investing in wedding photography insurance is an investment in your peace of mind. It allows you to focus on capturing those special moments without constantly worrying about what could go wrong. Don't wait until it's too late – get insured today!

:max_bytes(150000):strip_icc()/277019-baked-pork-chops-with-cream-of-mushroom-soup-DDMFS-beauty-4x3-BG-7505-5762b731cf30447d9cbbbbbf387beafa.jpg)